June Rail Industry Report

2022 Railcar Traffic

The U.S. economy through the first part of the year has been a confusing ride. High consumer and manufacturing demand is competing with multi-decade level inflation and lowered consumer savings rates. One will have to give. Railcar car loadings have been much the same, seesawing between promising and discouraging.

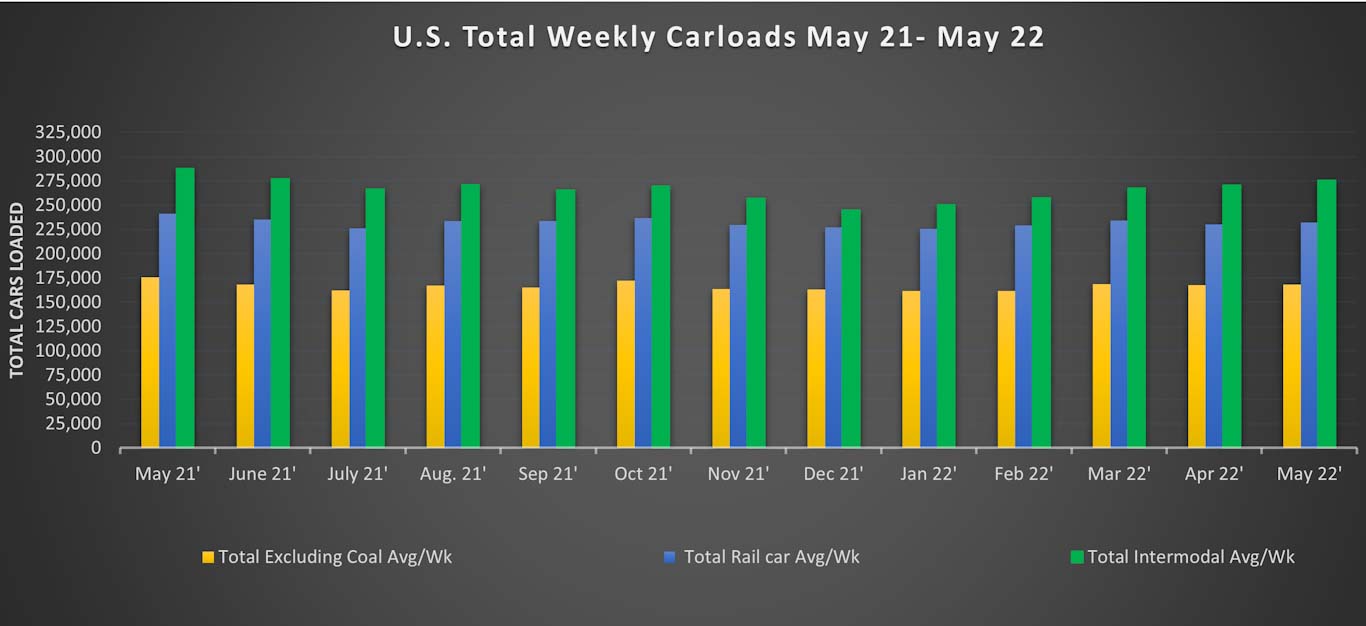

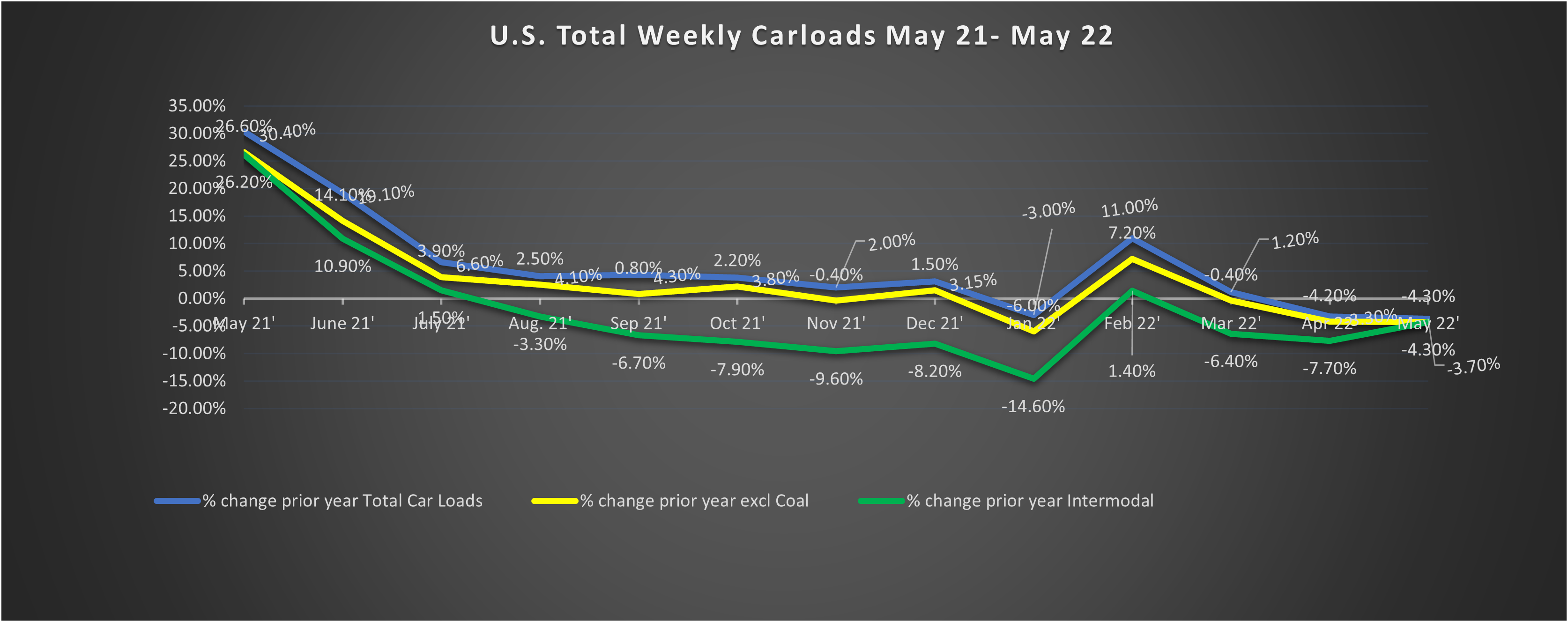

Through the first five months of 2022, total U.S. non coal railcar loadings are down 1.7% vs 2021. We are well below 2019 levels and not incredibly far above 2020. Especially considering where we were in early June of 2020. With the exception of February, which was lapping the 2021 Texas winter storm, every month in 2022 has been down over the same month in 2021.

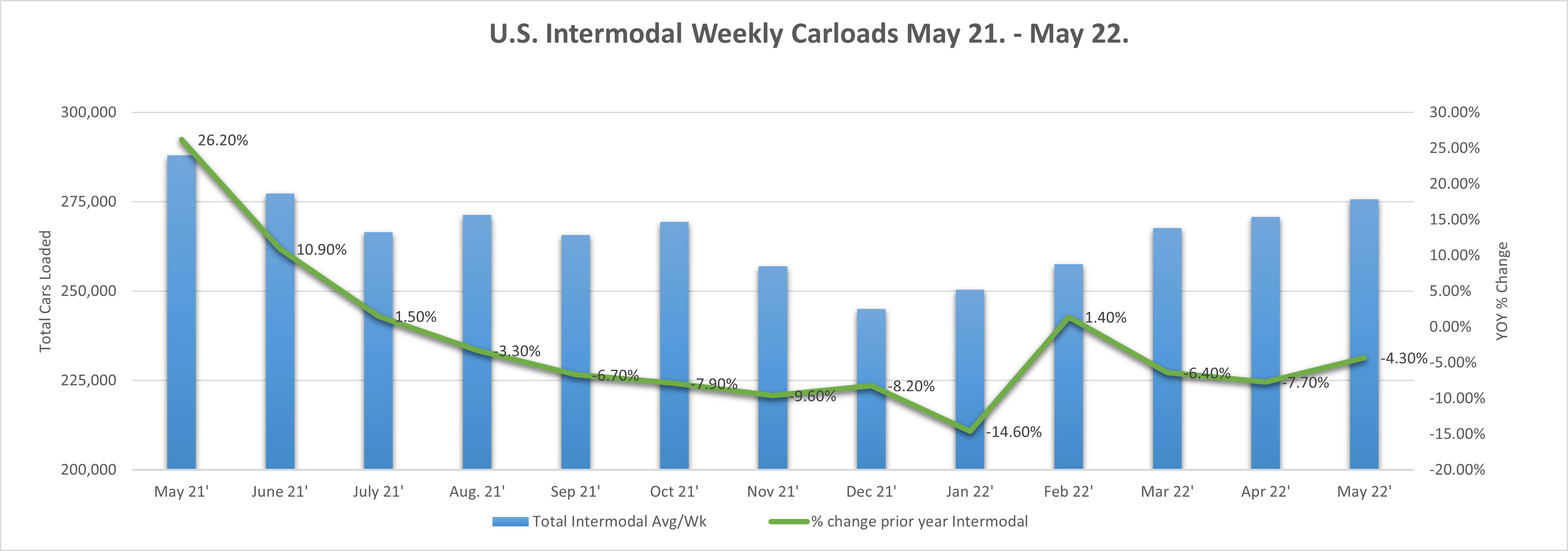

Intermodal loadings are much the same, down 6.6% year to date vs this time last year. Port congestion continues to be an issue as ship dwell times remain at elevated levels. Also, the recent COVID lockdowns in China have affected international shipping. We would caveat intermodal set records in the first half of last year, so the downdraft doesn’t sting quite as hard. Still, for a supposedly recovering economy, these are mixed signals at best.

So, if we are living in a post-pandemic world and there is apparently more demand than the economy can supply right now, why are railcar loadings down? Chew on this and we’ll come back to it.

Economy

To start, if loadings are down, is the economy as solid as we think it is? U.S. GDP for Q1 2022 was -1.5% quarter over quarter. Current estimates for Q2 are for +2.1% with annual estimates still ranging around 2%. That is in line with what many economists consider long term trend growth. It is well off of levels expected by an economy still recovering from a worldwide pandemic. As recently as last year, economists were calling for 2022 growth in the 4-5% range. We seem to be falling short of that mark considerably. Many reasons were given for the surprise slow down in the first quarter. Depending on the hue of your colored glasses, you could see the economy in a positive or negative light.

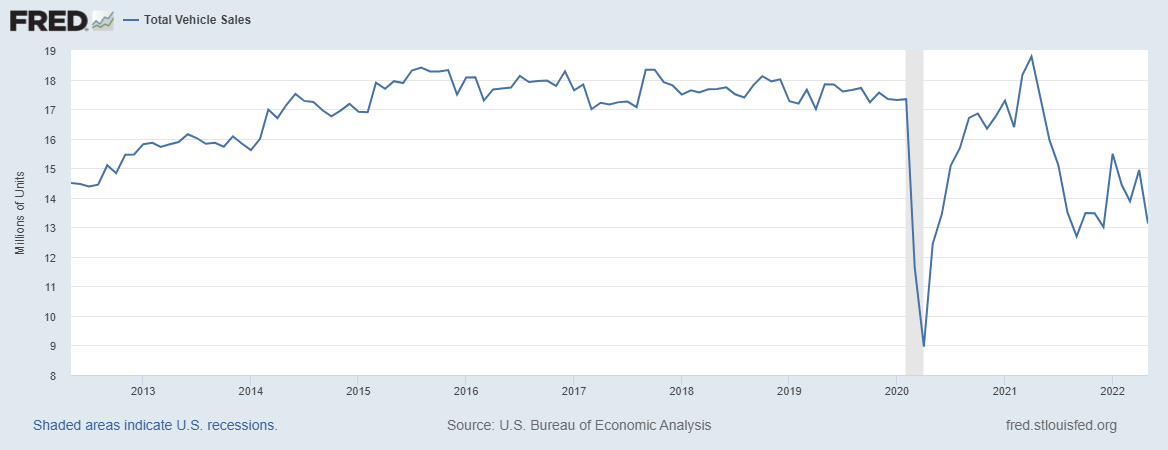

Highlighting the positive, personal consumption and expenditures were up 2.09%. A consumer-driven economy looks to this number first when measuring the recent health of the economy. That gain was entirely attributed to an increase in Services expenditures. While goods remained flat quarter over quarter, making up for losses in other categories, motor vehicles and parts, despite still low inventories, was a strong contributor. However, after stronger sales in Q1, May 2022’s annualized auto sales rate was back to just 12.7 million. A paltry number against an economy that was doing 17 or so million cars annually in the years prior to the pandemic. The increasing trade deficit was the largest single contributor to the slow down. Increased imports along with less total exports contributed to a 3.2% GDP percentage drop. Other decreases were related to reduced military and government spending.

As railcar loadings are almost strictly attributable to physical goods, the reduction in railcar loadings matches more closely with a flat goods sector reading. Likely the strongest indicator for the “good economy” camp is the still-robust jobs market.

Jobs Report | Employment

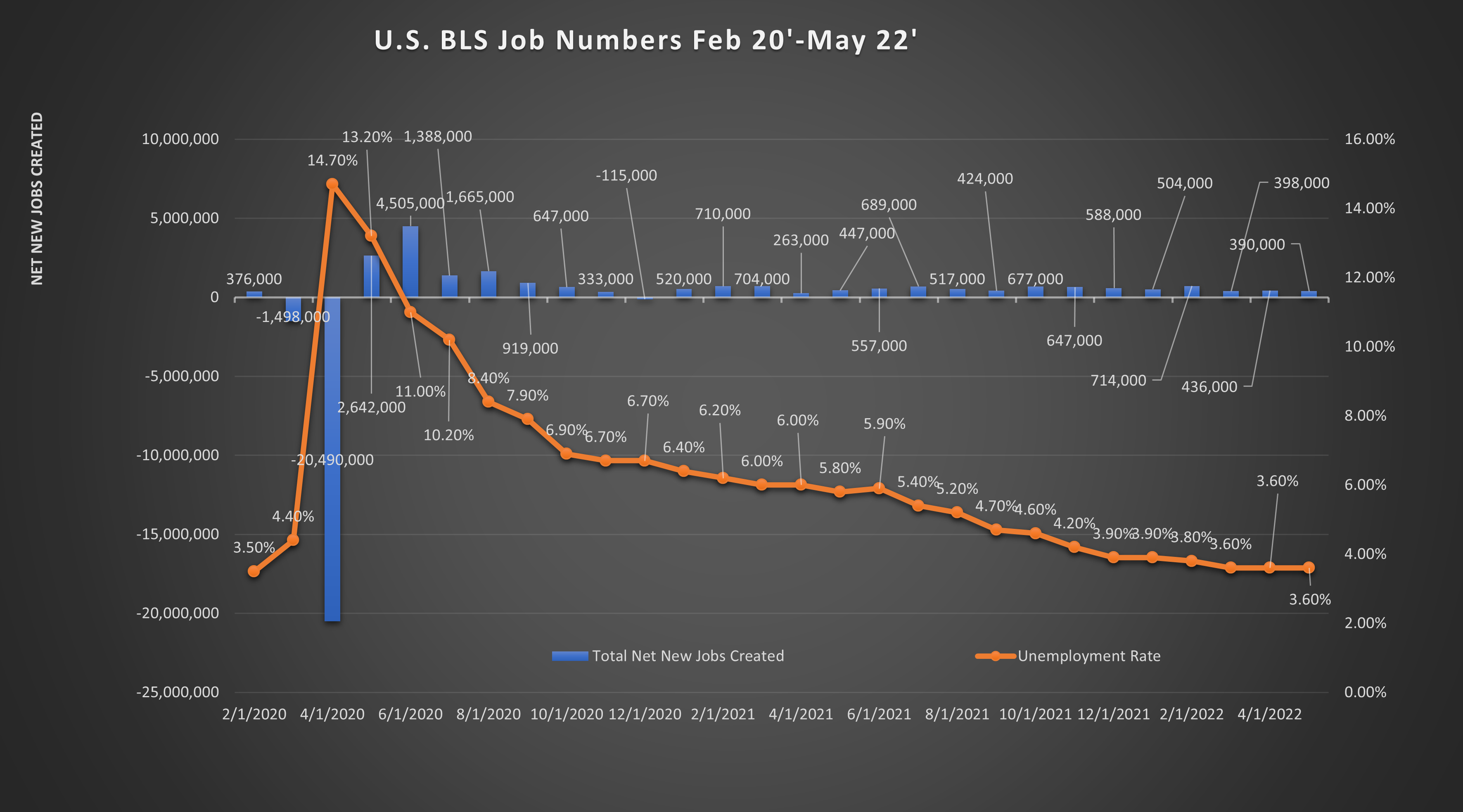

On June 3rd, the Bureau of Labor Statistics released its employment reading of a preliminary 390,000 net new jobs created in the month of May. With this report, the headline unemployment rate is now at 3.6%, just about back to 3.5% recorded in February 2020 before the pandemic.

That said, the total net new jobs created since May 2020 now totals a little over 21.1 million jobs. In March and April 2020, 22 million jobs were reported lost. We are still at 819,000 fewer total jobs than before the pandemic. So how can we have 3.6% unemployment? As we have discussed before, the unemployment rate measures those working or actively seeking work. Millions of jobseekers fell off the board during the pandemic. Whether early retirements or marginal workers who have yet to come back to the labor force, we have a labor force participation rate of 62.3% as of May 2022. In February 2020, the LFPR was 63.4% just over a full percentage point higher. How many missing workers does that equate to? A May Kansas City Fed article cites approximately 2 million less workers are still missing from the workforce as compared with 2019 levels.

We point out this number specifically because we feel it is one of the best comparisons for the reported unemployment rate vs the total number of people working. It also lends an explanation to how an economy considered at near “full employment,” less than 4% unemployment, can keep adding 400K+ jobs per month. It is largely workers coming back into the workforce. The take away from that being that the labor market may still have some room yet to expand and produce more jobs.

Further complimenting the employment train, on June 1st, the Bureau of Labor Statistics released its “Job Openings and Labor Turnover” survey for the month of April. On the last day of April, there were 11.4 million jobs available in the U.S., down slightly from the record March. It is almost twice the number of jobseekers currently considered in the unemployment rate. If we may add one small bit of anecdotal commentary, a high jobs/unemployment ratio often means companies cannot find people with the skills required to fill their position needs. While this creates inefficiency in the markets, the longer this goes on, the more willing companies will be to train people with new skills to meet these roles. This increases the overall productivity of the labor force and equips people with new skills they will carry with them going forward.

With more people working and bringing home incomes, the economic optimist will posit inflation will eventually tamp down but these new jobs will carry forward.

Inflation | Savings Rate

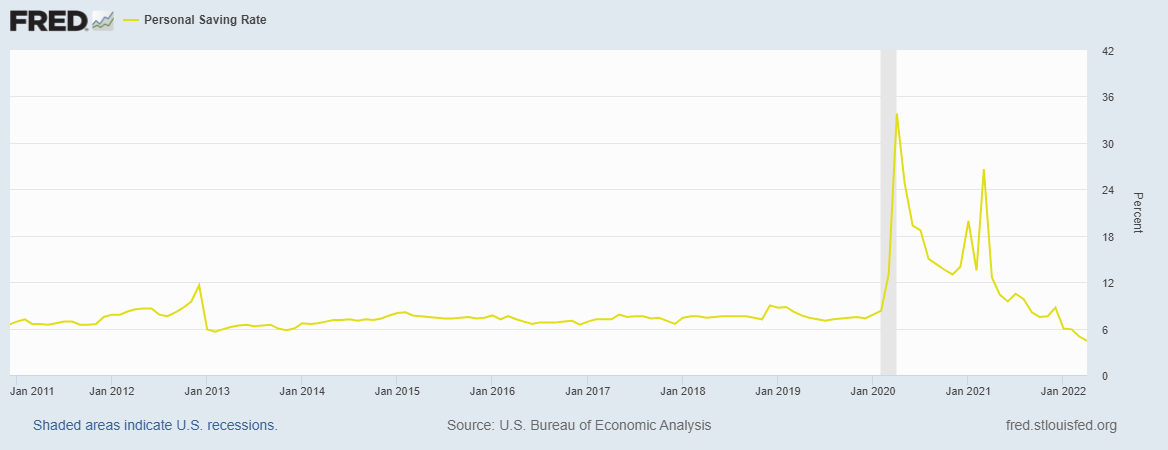

A strong labor market combined with still largely positive economic surveys point toward a fairly rosy picture. The pessimist's case revolves around inflation and fast dwindling consumer savings rates. You may remember in March 2021 State of Rail Report we reported consumer savings rates had reached near record levels. A combination of government helicopter cash and lockdowns preventing spending left consumers with full piggy banks and a lot of pent-up demand. While that pent-up demand has not yet shown major signs of slowing, as highlighted by the consumer spending we mentioned above, the cracks are beginning to show. The April personal savings rate as reported by the Bureau of Economic Analysis was down to 4.4% in April 2022. It has been ticking down month after month and has now reached below long term levels. As consumers have less in savings, they traditionally turn to credit sources like credit cards and home equity loans before eventually reducing spending habits. You can see this in the federal reserve’s June 7th consumer credit report. In April, revolving credit, which is mostly credit cards, increased at an annual rate of 19.6%. That is in addition to March’s 29% reading. That means the amount of short term credit like credit cards consumers took out increased about 40 billion dollars in April.

The other headwind for the economy: inflation. Inflation remains at or near multi-decade highs. As we have not seen inflation like this since the Carter 70s and early 80s, or 40+ years for those keeping score at home, many consumers have never experienced an environment like this. Inflation as reported by the Consumer Price Index in April 2022 was 8.3% year over year - a small drop from the March high of 8.5%. Inflation is in everything too, with some standouts over the past year. Food is up 9.4% year over year, energy is up 30.3% with gasoline up over 43% in a year. Not to be lost in the energy shuffle, it is not just transportation energy - electricity is up 11.0% over April 2021, utility gas service (natural gas) 22.7%. The increases in basic expenses hit consumers right in the pocketbook and limit the amount of discretionary income remaining for purchases and services like dining out.

Included in the BLS labor report, average hourly earnings are up 5.3% over the past twelve months. Compared with an inflation rate of 8.3%, that means real wages in terms of purchasing power have gone down over the past twelve months. If inflation does not dissipate, workers will continue to see their dollar carry less power going forward.

Housing | Autos

Speaking of that lower purchasing power: another indirect effect of inflation is increased loan rates for purchases by way of rate increases by the federal reserve. This affects all parts of the industrial and consumer economy. For companies, it means a higher cost of borrowing for investments into new equipment and expansions. For consumers, it means higher loan rates for purchases, specifically homes and autos. We mentioned before that new auto purchases for May were reported at a seasonally adjusted 12.7 million annualized new light vehicles sold.

Pricing and vehicle availability certainly play some role in that, as used and new auto prices are both up double digits. Interest rates also play a huge contributing role. The average new car payment in Q1 2022 reached a record $648/month. That is largely before many interest rate increases started taking place. In what may be a small blessing, the slow down in vehicle purchases may give dealerships time to restock inventories that have been severely depleted for more than a year. Increased inventory should help to lower the pace of inflation.

A better example of how interest rates affect the greater economy: Housing. New housing starts in April were still near multi-year highs at 1,724,000. That is near the highest since pre-2008 recession. It’s important to remember the largest U.S. generation ever, millennials, are now well into their prime family-forming years. That, combined with a 2010’s decade that saw the lowest housing building levels in decades, created an enormous amount of pent-up demand. That demand hit flood proportions during the pandemic as millennials traded in the city for suburban living and smaller cities.

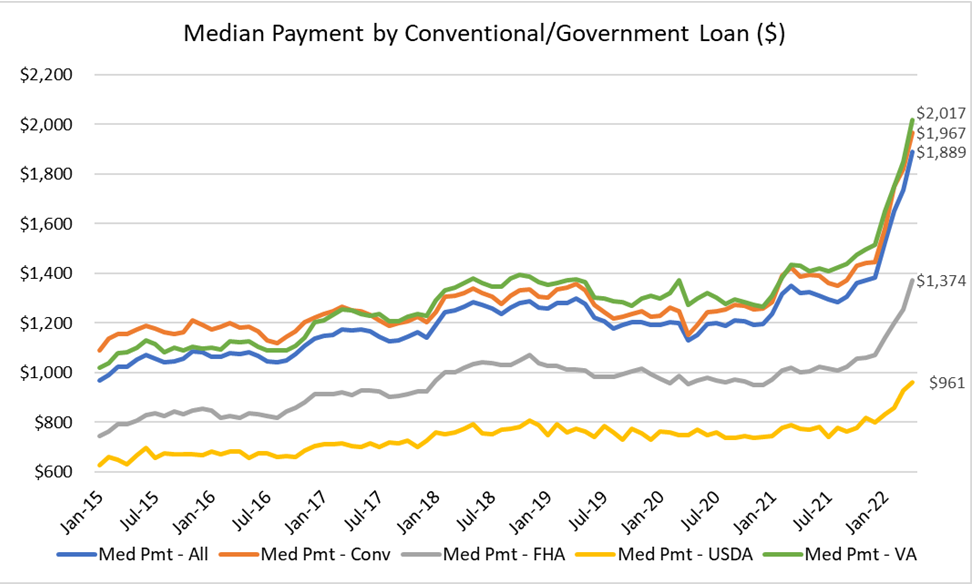

What does that have to do with interest rates? In just a few months, mortgage rates have gone from historic lows to 12 year highs as cited by a Reuters article on May 18th. On May 26th, the Mortgage Brokers Association reported the average median mortgage payment in April 2022 was $1,889 from $1,736 in March - an average payment increase of 8.8% in just a month. Compared with a year before, the typical principal and interest payment has increased by $569 dollars/month. That’s a car payment right there. We discussed rapidly rising home prices before, combined with increases in mortgage loan rates, home affordability continues to go down month after month.

If this report has a theme it is cracks. The forward looking indicator for the housing market is permit applications for future builds. The cracks may be first showing here. New building permits dropped 3.2% in April. Also, while housing starts remain high, the percentage of multi-family starts (apartments) is becoming a larger percentage of total new starts. Of that 3.2% total drop, single family home permits dropped 4.6% while multi-family permits dropped just .6%. Remember, this is April data and the prices and rates have continued to rise since.

Going back to our consumer economy point. The more consumers spend on basic necessities like food, housing, and transportation, the less they have to spend on consumable goods. The same goods that travel in railcars.

Railcar Categories

Through May 2022 total ex-coal railcar loads are down -1.7% from this time in 2021. That is the fewest number of railcars since before 2013 excluding 2020.

Chemical car loadings are the single biggest commodity category excluding coal. In May chemical loadings were down 1.4% vs May 2021. Chemicals overall this year are still up 6.6% from 2021. Chemicals have been a standout bright spot over the past several years as a growing part of the U.S. economy.

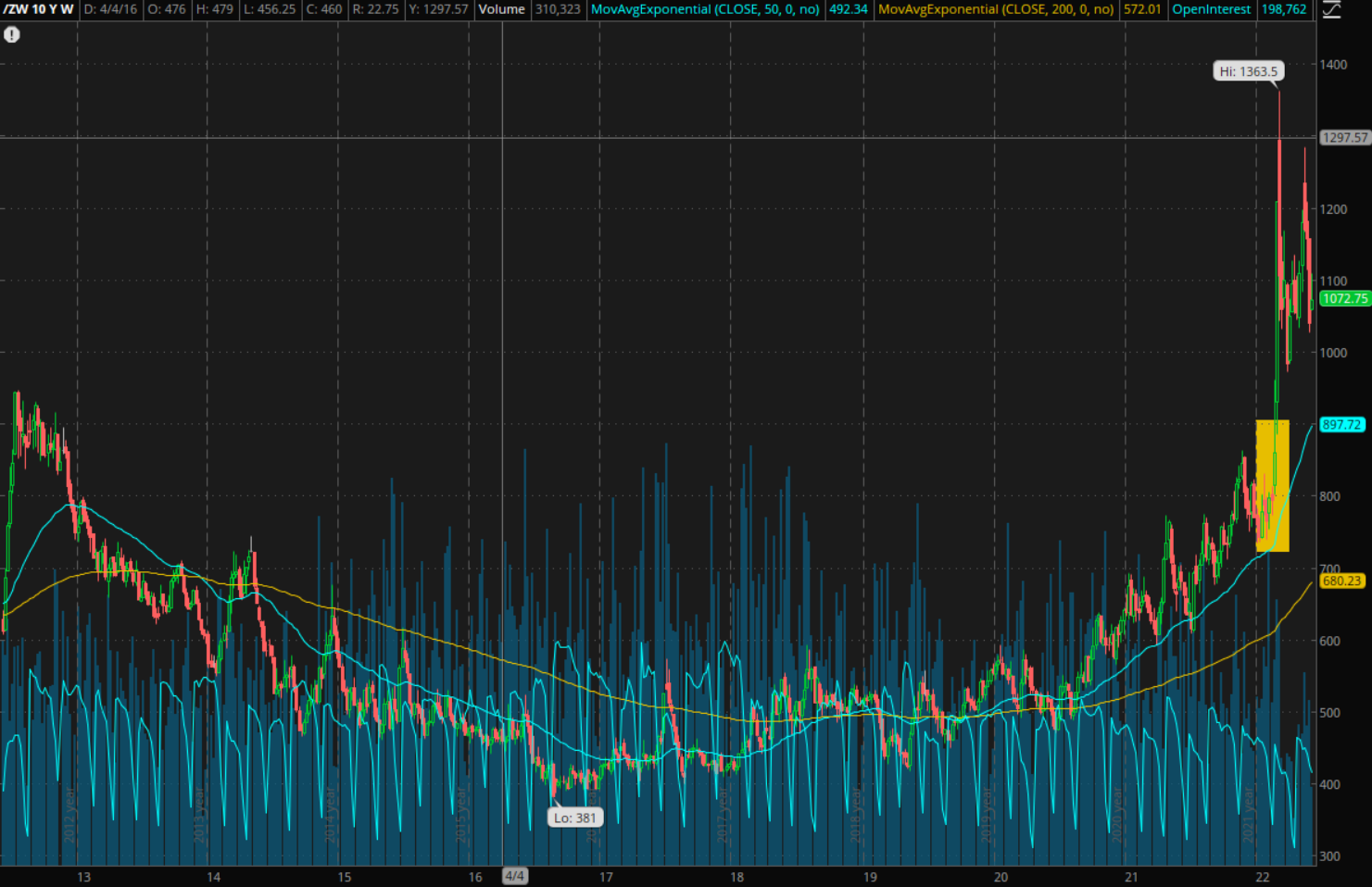

Grain (Corn, wheat, soy) loadings for 2022 are down -10.3% compared with 2021. That said 2021 was a record year for grain loadings. We are still near historic highs. Where grain goes the rest of the year will be interesting. You have probably seen a report by now calling Ukraine the bread basket of Europe.

This is clearly indicated by the 10 year wheat futures chart here. The yellow section highlighted is around February 24, when the Russian army moved into full scale invasion of Ukraine. As you can see wheat was already at multi year highs before skyrocketing around the beginning of the invasion. It has retraced some, but seems to be forming a base around the $1,050 level. That would be a sustained level higher than anything seen in the last ten years.

One commodity category beneficiary of higher oil prices is crushed stone, sand, and gravel. These are used primarily in the fracking. Year to date this commodity category is up 10% over 2021. May was the highest volume month since later 2019. The Baker Hughes rig count corroborates this increase as the rig count has increased by over 30% in a year as of the last reading. Hopefully these additional rigs will add some supply to the market and start cooling off gas prices.

Perhaps not though, May 2022 petroleum products were down 13.5% from May 2021. This speaks more to where oil is produced in the U.S. most oil production moves by pipeline. Still The EIA does not expect U.S. crude oil production to return to 2020 levels until well into 2023. Expectations for 2022 are around 12 million barrels per day produced.

Industrial products, a combination of 7 industrial facing rail commodity sectors is the most historically correlated with GDP. Through May 2022 car loads of industrial products have totaled just over 1.9 million car loads. That is up 1.8% through may 2021, but the lowest reading in almost ten years excluding 2020 and 21. We are still off the roughly 2 million car load mark we have been at through most of the 2010’s.

Andress Engineering Associates will continue to be here to support our customers with Trackmobile™, Modjoul™ smart belt, compressor, crane, and chiller needs.

Andress Engineering Associates has over 60 years as a Trackmobile Railcar Mover dealer and industrial Engineered equipment systems provider. We remain open and ready to support the operations of our customers. We have a fleet of Trackmobiles available for rental. Our service technicians are available 24/7/365. Our Trackmobiles, cranes, and compressors operate in some of the most critical industries supporting our economy. Our team stands ready to support your application in any way we can.

Sources: