March in the Rail Industry

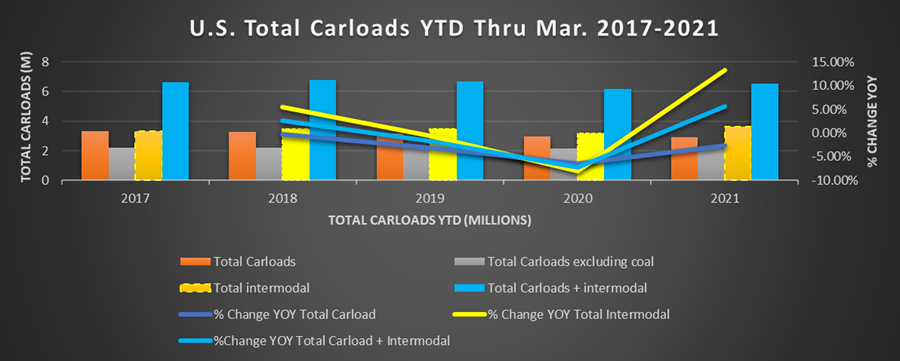

First Monthly Total Carload Gain Since January 2019

March marks the one-year monthly anniversary of the Covid Pandemic. It was in March last year that the first U.S. lockdowns largely took effect. As a result of that, we are entering a time that will see some unusual year-over-year statistics. In March 2021. U.S. total carloads were 4.1% higher than they were in March 2020. Notice we said total carloads, not total carloads ex-coal. Which our regular readers will site as the statistic we most often reference. Ex-coal carloads were actually only up 2.9% over March 2020. Intermodal carloads on a weekly average were 286,066 cars per week; up 24.0% over March 2020. Yes, you read that correctly. Like we said, some outlier numbers.

Railcar Loadings Analysis:

An economy that has been squeezed by the stranglehold of the pandemic for the last year feels ready to burst. Commodity prices are more than double what they were a year ago for many products. The rail industry seems to be echoing the same sentiment. So far, the winter storm shutdowns of February seem to have been transitory. As Grain, coal, and motor vehicle parts lead car loadings gains in March. For those thinking the intermodal numbers are just a measure of a weak March 2020. March 2021 intermodal loadings were 8.0% higher than in March 2019. When the economy was arguably the strongest it’s been in decades. A year of shutdowns combined with unprecedented government spending has clearly built-up demand.

Overall this year, total carloads are down -2.6% through March 21 compared with the first three months in 20. Ex-coal carloads are down -1.5% YTD. Remember shutdowns didn’t begin happening in earnest until March though. Those comparisons are expected to sharply rise in the coming months.

Highlight categories:

In March, 11 of the 20 AAR carload commodities posted year-over-year gains. By comparison, It was three in the winter storm-riddled February.

Grain has been no stranger to this report. March was no different. Up 22.1% over March 2020. Grain carloads for the first quarter of 2021 were up 25.5% over Q1 2020. That’s two straight quarters of 25%+ year-over-year growth, and remember those are almost strictly non-Covid comparison months.

Coal has been talked about in this newsletter but rarely in a positive light. Overall coal loadings have been declining precipitously over the last decade. Power plants in the U.S. have largely converted to natural gas and other production sources for power. In March 2021 though, coal loadings were up 7.6% from March 2020. It’s a small respite for those in the coal sector. Coal loadings are still down 40% from just 2018.

Car and autos have rebounded significantly from 2020. Posting a 16.4% gain over March 2020. However, our news followers have heard of the semiconductor and parts shortages affecting automobile production. In recent weeks, major automakers like Ford™ and GM™ have been forced to reduce shifts and hours for lack of supplies. Stories like this make market watchers more and more present-minded of the dreaded word Inflation. We’ll have more on that in an upcoming reopening-focused article.

Touching further on that. Lumber and wood products only rose 1.4% over March 2020. Despite the fact that lumber prices are double what they were a year ago. We touched on a similar issue with Steel prices in our January/February rail report.

The Economy:

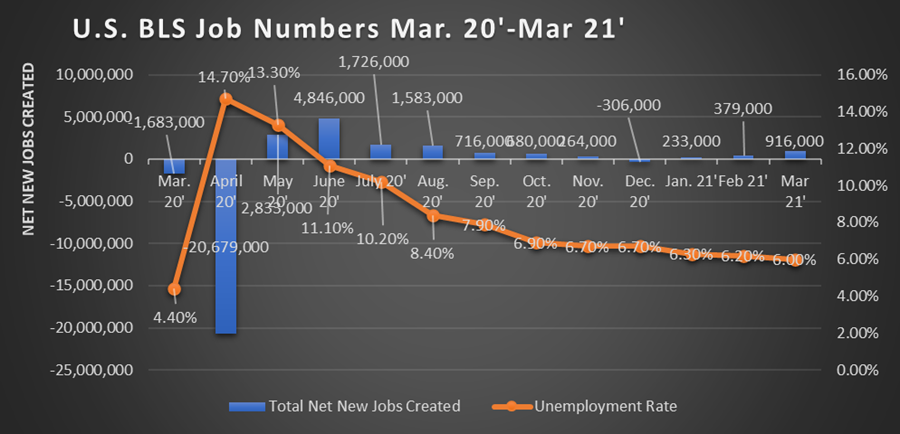

Jobs in March 2021. The U.S. economy generated 916,000 net new jobs. The best reading since August 2020. In addition, revisions added an additional 156,000 jobs to the previous January and February reports. That brings the unemployment rate to 6.0%. Leading the charge were the leisure and hospitality sectors which added 280,000 net new jobs. In pre-pandemic times. 280K net new jobs would be considered a great month by itself. The lifting of restrictions in states clearly contributed to this month. Industrial sectors that tend to correlate to railcar loadings were also strong in March. Manufacturing increased 53,000 jobs in March. Construction added 110,000 jobs. In the housing boom that we are currently seeing. Those workers are greatly needed. We expect to see a further gain in the construction sector in the upcoming months.

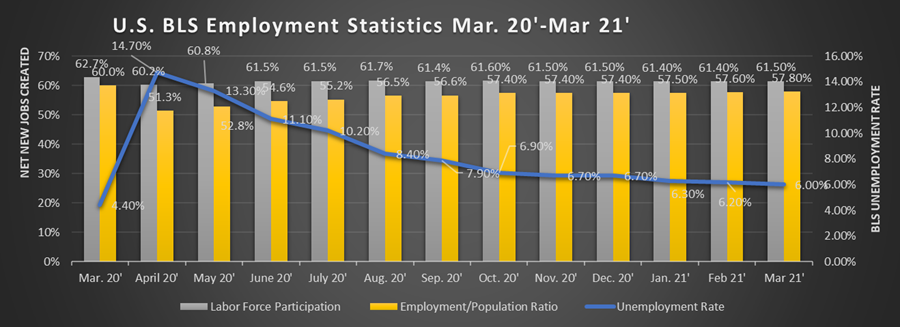

No one is implying the work is done, but we’ve mentioned a glimmer of light at the end of the tunnel in previous months. That light definitely seems to be getting brighter. While 6.0% unemployment is 2.5% higher than it was in February 2020. It is a far cry from the 14.7% high of April 2020. The labor force participation rate or percentage of able-bodied prime-age working adults in the U.S. is still two full points from where it was in February 2020. That implies there is still a lot of slack in the labor force to meet increased demand for goods and services.

Through March 2021 we have regained just under 14 million of the 22 million net jobs lost from the pandemic and government shutdowns. That leaves us with about 8.5 million fewer jobs than in February 2020.

Economic Indicators:

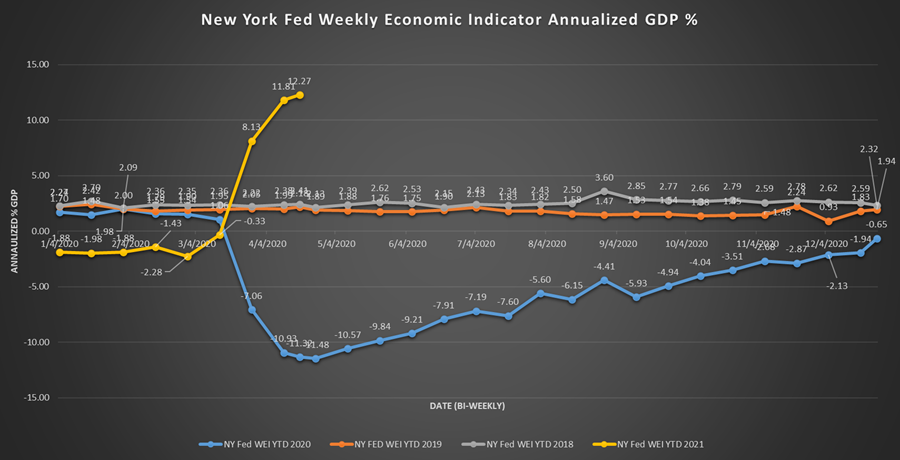

We touched lightly on inflation in our rail sector. We also said this felt like an economy ready to bust out of the gate. The New York Fed’s weekly economic index reported a growth rate of 2.90% for the month of March. Those numbers are accelerating quickly going into April. March 2021 is the first positive reading we have seen since the pandemic began. U.S. GDP for the first quarter of 2021 will be reported at the end of April. Current estimates are tracking it at around 6.0%. if that is true it will be the highest reading in almost 20 years excluding Q3 2020 which was artificially high for pandemic reasons.

While the Government may have been spending at precipitously high levels the last year, American citizens have been saving at unprecedented levels. Look for a special article on the Pandemic reopening in the coming weeks. We will dive into this much more deeply. American savings rates as of February were just over double what they were only a year ago. As things reopen, pundits are betting Americans will be jonesing to spend those savings and return to pre-pandemic activities like traveling and eating out.

Other economic indicators are all pointing to similar signs.

Autos and Housing:

In March new auto sales were at a seasonally adjusted pace of 17.7 million vehicles. That is the highest monthly sales rate since October of 2017. Remember we said automakers are facing supply shortages too. Leading to sharply higher prices in both and used autos.

We don’t need an article to see housing is increasing right now. Ride around in any metro area and you’ll see new construction going up. Housing starts in March were reported at an annual rate of 1.739 million. That is up 19.4% from February. It is up 37% from March 2020. Housing is considered one of the biggest economic indicators. New housing especially single-family implies other consumer expenditures as families fill and furnish these homes. That means couches, chairs, TVs, etc… All goods that regularly come in intermodal trailers. With such a supply-demand imbalance in housing right now, housing prices have risen dramatically over the last year. Leading many to question where the line for affordability is going to be drawn. Also how quickly can new supply alleviate the strain that’s on the housing market? We look forward to monitoring this in the coming months.

Federal Reserve Weekly Economic Index:

We always close with our economic index. The W.E.I. has turned positive! For the first time since the pandemic and this tool was put together. Further, as we have moved into April. It only continues to gain steam. Train joke, lol. Reporting a 12.27% rate for the week ending April 17. We realize that is against incredibly weak 2020 comparisons, but it is still nice to see the ledger on the positive side for a change.

>

We will continue to be here to support our customers with Trackmobile™, Modjoul™ smart belts, compressors, cranes, and chiller needs.

We have over 60 years as a Trackmobile Railcar Mover dealer and industrial Engineered equipment systems provider. We remain open and ready to support the operations of our customers. We have a fleet of Trackmobiles available for rental. Our service technicians are available 24/7/365. Our Trackmobiles, cranes, and compressors operate in some of the most critical industries supporting our economy. Our team stands ready to support your application in any way we can.

We have a fleet of Trackmobiles available for rental. Our service technicians are available 24/7/365. Our Trackmobiles, cranes, and compressors operate in some of the most critical industries supporting our economy. Our team stands ready to support your application in any way we can.