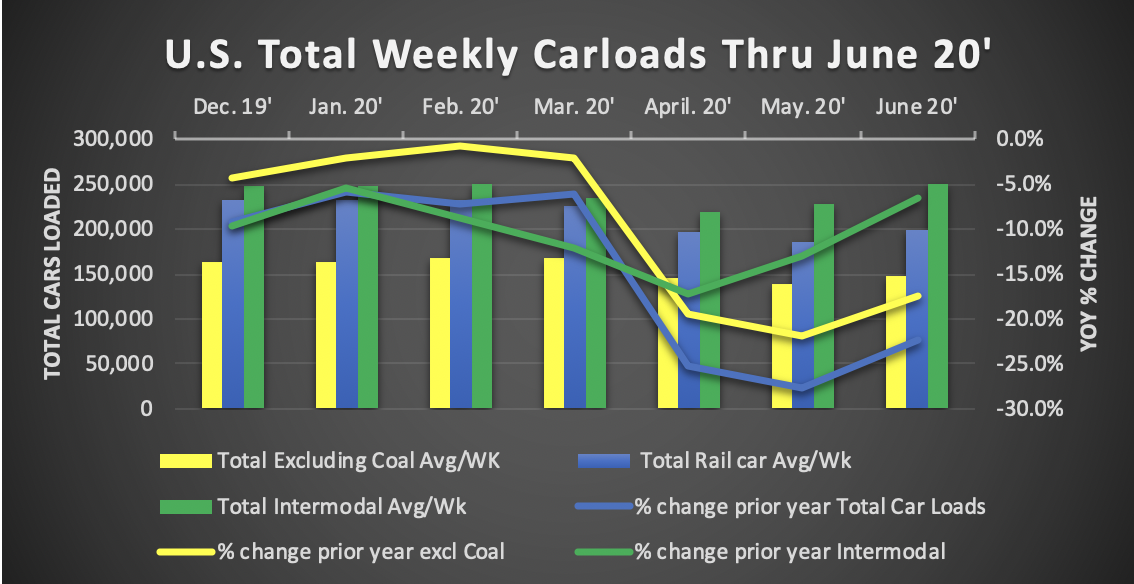

June Railcar Loadings

Total U.S. railcar loadings improve from May lows in June. Still well off 2019 levels.

June's total U.S. Railcar loadings saw a decline of 22.4% over June 2019. While a terrible mark in any other circumstances, this marks a small rebound from the 25.2% April decline and 27.7% May decline. As U.S. economies continue reopening, industries are hopeful May will mark the lows.

Railcar shipments continued to be weak in June. While weekly car loadings improved from the lows of April and May; weekly loadings were still down 22.4% compared to June 2019. Excluding coal shipments, which continue to decrease as coal power production drops across the U.S car loadings were down -17.4% in June. Again, better than April’s -19.4% and May’s -21.9%, but nothing to write home about. One bright spot, intermodal loadings bounced back significantly. “Only” down -6.6% from the same period one year ago.

June brings the 2020 total rail car loadings to -15.9% compared to this time last year. -10.8% excluding coal and -13.2% for total cars + intermodal.

The economic shutdown and its effect on rail car shipments can be seen with even more clarity when looking at specific sectors. Housing starts since COVID have dropped to a level below one million. Reported starts in May were for SAAR of 974,000 in May. January and February both reported SAAR rates of over 1.5 million. Accordingly, U.S. & Canadian carloads of lumber and wood products YOY were down 8.8% in June, 19.3% in April, and 19.0% in May. Primary metal products were down 30% YOY in Q2 2020. Other sectors have seen similar results.

Economic Indicators:

As we covered in our piece last week. Some economic indicators have indicated the recovery is moving forward, but provide a mixed picture. Also, rising cases again have slowed or paused many states reopening plans. The Bureau of Labor Statistics June jobs report showed the creation of 4.8 million net new jobs. This lowered the official unemployment rate to 11.1% and smashed analyst expectations for a consensus of 2.9 million new jobs. A slew of other positive or at least less negative economic indicators have been released.

Last Thursday, July 2, 2020, the U.S. Commerce Department’s new orders advanced 8.0% in May. Non-defense capital goods excluding aircraft increased 1.6% in May after a -6.6% decline in April. On Monday, July 6, 2020, the Institute for Supply Management reported that its Non-manufacturing index advanced to 57.1% in June. Anything over 50 indicates the service sector is in expansion. May’s reading was 45.4 and analysts were expecting a reading of 50%.

NY Fed Weekly Economic Indicator

Andress Engineering has over 60 years as a Trackmobile dealer and industrial Engineered equipment systems provider. We remain open and ready to support the operations of our customers. We have a fleet of Trackmobiles available for rental. Our service technicians are available 24/7/365. Our Trackmobiles, cranes, and compressors operate in some of the most critical industries supporting our economy.

customers. We have a fleet of Trackmobiles available for rental. Our service technicians are available 24/7/365. Our Trackmobiles, cranes, and compressors operate in some of the most critical industries supporting our economy.

Our team stands ready to support your application in any way we can.